W.A. Robinson: Important COVID-19 Announcements & Information READ MORE

Canada’s mortgage industry changed in 2018 as the impact of higher interest rates and stress tests reverberated across the country, decreasing housing affordability. In general, this resulted in increased monthly mortgage costs and reduced purchasing power.

While these changes affected many existing homeowners and prospective buyers, they were likely felt most acutely by first-time homebuyers, who faced increased obstacles to making their first purchase.

While circumstances can change quickly in a market with countless variables at play, our current expectation is that 2019 is going to be challenging – both for first-time homebuyers in Canada and for the mortgage brokers assisting them.

Here’s why:

After hovering near zero for an extended period, interest rates have risen significantly in the past two years. The Bank of Canada increased its policy interest rate from 0.5% in July 2017 to 1.75% in October 2018 (the most recent change), which in turn has boosted mortgage rates. While this has put a chill in the market, it has also increased the interest component of mortgage costs.

According to a December 2018 housing affordability report from RBC, homebuyers in Toronto required a whopping 75.3% of the median household income to cover annual homeownership costs in the third quarter of 2018. Prospective homebuyers in Ottawa faced a much more reasonable level at 38.6%.

December 2018 housing affordability report from RBC

“Despite the market-cooling effect of rising interest rates and stress tests, housing affordability continues to deteriorate.”

However, for both cities, the third-quarter figures were up 0.3 percentage points from the second quarter. In other words, despite the market-cooling effect of rising interest rates and stress tests, housing affordability continued to deteriorate. Meanwhile, interest rates are expected to continue to rise gradually going forward and further weigh on housing affordability in 2019.

From a policy perspective, recent measures aimed at cooling down the real estate market appear to be working. The double impact of rising interest rates and mortgage stress tests have generally stemmed the rapid rise in house prices.

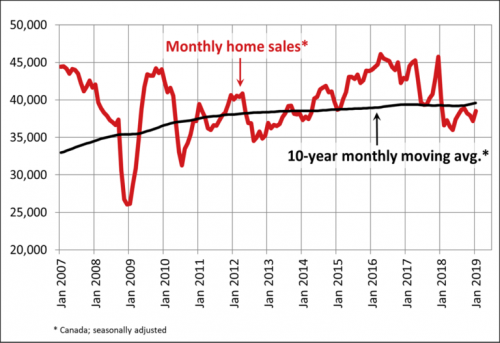

According to the Canadian Real Estate Association, the national average sale price saw a 4.9% year-on-year drop in December 2018 while the year ended with four straight months of declining national home sales.

Canadian home sales fall further in December

Yet even in a softer market, first-time homebuyers are still being squeezed.

Unless they have money for a 20% down payment – which is often a stretch for first-time buyers – they are required to have mortgage insurance to access funds from big banks. This requires the stress test to be applied, which puts them at a considerable disadvantage in terms of buying power compared to well-capitalized buyers.

There are various policy solutions circulating in the market, such as:

The former would reduce uncertainty by standardizing requirements for all mortgages; the latter would help to make monthly payments more affordable.

Those aiming to purchase their first property could also benefit from shifting their expectations.

Previously, the hunt for an affordable foothold in the property market saw prospective buyers turn from single-family homes to condos. Today, some Canadians are shifting focus again and turning to rural properties in their pursuit of affordability.

Another solution?

First-time homebuyers (or their mortgage brokers) can seek out alternative lenders able to offer solutions that are unavailable from the big banks.

From name recognition to attractive rates, there are various reasons for prospective homebuyers and their mortgage brokers to look to Canada’s big banks for their mortgage needs. Yet B lenders and other private lenders are crucial for filling gaps in the market.

For first-time buyers discouraged about their home-buying prospects in 2019 amid deteriorating housing affordability, alternative lenders offer hope.

For example, Pillar’s uninsured mortgages mean borrowers do not face the same stress tests required by big banks (borrowers are required to qualify with a reasonable TDS), which can boost their maximum loan amount. In addition, Pillar can provide 30-year amortization, which can be useful for lowering borrowers’ monthly payments.

Pillar’s team works closely with Ontario’s mortgage broker community to provide solution-based lending for borrowers with needs outside the norm. While clouds remain on the horizon, we stand ready to help brokers navigate the challenging mortgage landscape so that they can bring the joy of first-time home ownership to more clients in 2019.

copyright © 2024