Top Picks

If there’s any indication that we’re entering a new chapter, it’s this. After cutting interest rates early on in the pandemic, the Bank of Canada has implemented another rate hike aimed at stemming inflation – and it’s a big one. Read our latest article to learn what it means for you and your clients, plus access resources to navigate lending in today’s construction market.

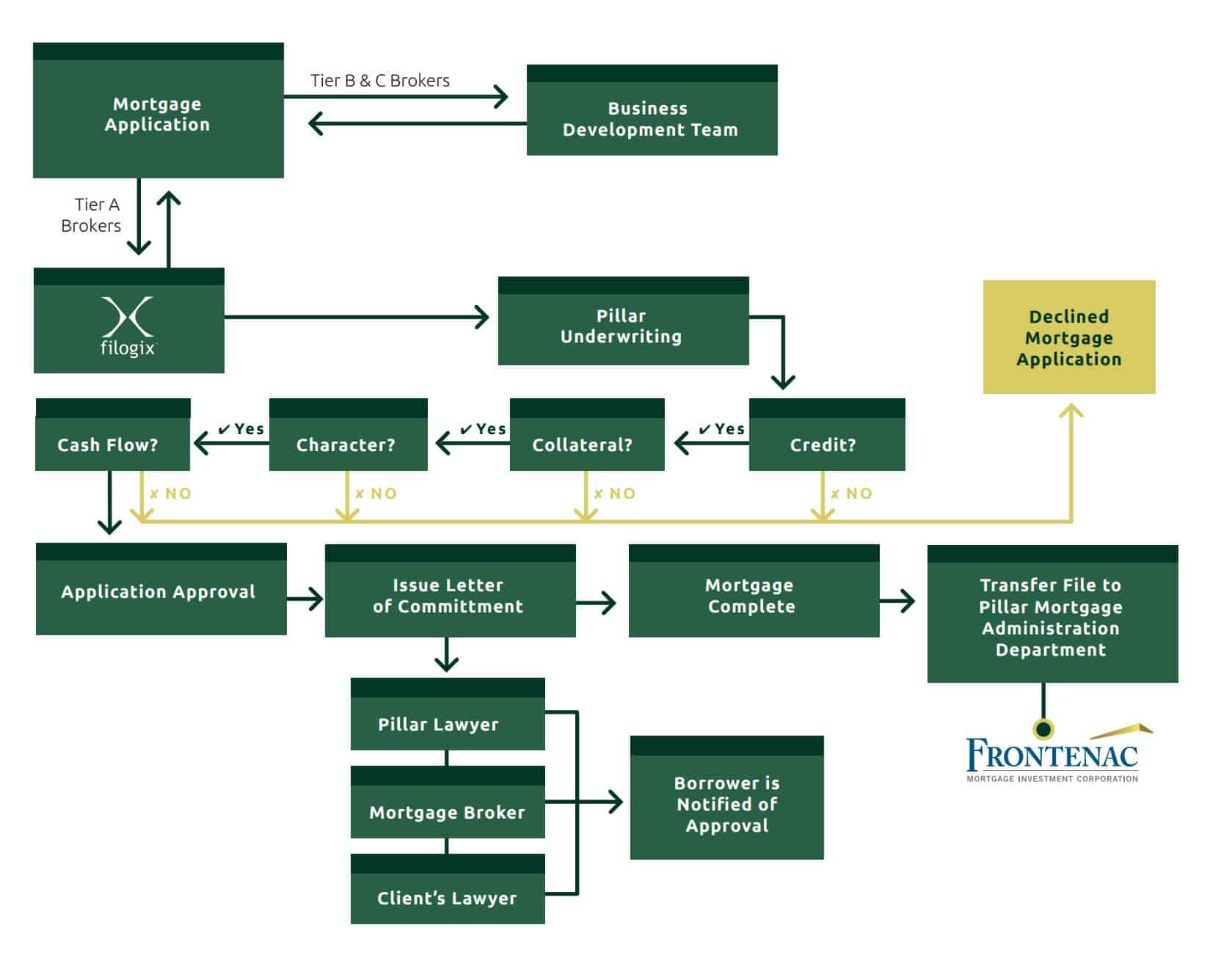

A framework of the construction project process.

For Brokers and Borrowers

All Documents

All Articles

The lights may shine bright in the big cities, but there’s plenty more to Ontario than urban centres alone. In our vast rural landscape, diverse property types and intricate client needs mean you might encounter lending scenarios you wouldn’t otherwise in the city. At Pillar Financial, we pride ourselves on being focused on rural properties […]

Construction Articles

The lights may shine bright in the big cities, but there’s plenty more to Ontario than urban centres alone. In our vast rural landscape, diverse property types and intricate client needs mean you might encounter lending scenarios you wouldn’t otherwise in the city. At Pillar Financial, we pride ourselves on being focused on rural properties […]

Residential & Rural Articles

The lights may shine bright in the big cities, but there’s plenty more to Ontario than urban centres alone. In our vast rural landscape, diverse property types and intricate client needs mean you might encounter lending scenarios you wouldn’t otherwise in the city. At Pillar Financial, we pride ourselves on being focused on rural properties […]

All Frequently Asked Questions

Construction Frequently Asked Questions

Residential & Rural Frequently Asked Questions

Self-Employed Frequently Asked Questions

All Frequently Asked Questions

During the construction process we do not take a regular mortgage payment. Interest accrues and is taken from each progress advance. In cases where there may be more than 45 days between draws, we may request to take an interest only PAC payment to keep the interest from getting too high for the client and therefore the PAC form assists with the collection of these payments.

FMIC (Frontenac Mortgage Investment Corporation) is the lender (fund); FMIC has a requirement through its prospectus to hold assets by a trustee - That is Computershare; Pillar has an administrative agreement with FMIC where it underwrites and administers all mortgages for them.

As a short-term lender, our focus is improve the financial situation of our clients. Upon completion of a build it is in the best interest of our clients to move to a lower rate more traditional mortgage.

One of the most important parts of each file is our collateral and we want to ensure that we have supporting value in the subject property to protect our investment.

When requesting all pages of each document, this is our effort to verify the validity of documentation in order to prevent fraudulent activity.

Yes, we will consider clients who are currently in a Consumer Proposal, but the balance of the proposal must be paid either prior to funding or from the proceeds of the financing.

We do offer financing on clients with fully discharged bankruptcies.

Our policy requires a Phase One to be completed on all files where there is a commercial component or zoning on the property is listed as “Commercial” to check for any environmental concerns on the subject property. Eg. Mixed-Use, Commercial Vacant Land.

No, we are only able to register in first place.

We currently lend in all of Ontario.

It is required to be spelt out as it is the "Legal Registered Name".

It is an internal policy to ensure that no executions have been placed on any of our clients province-wide as that is our current lending area.